FinTech Trends 2026: How top FinTech trends are shaping digital banking after 2025

FinTech trends 2026 are moving from hype to production as blockchain payments, tokenized assets and smart contract automation reshape real-world finance. This guide from Dmytro Nasyrov, CTO at Pharos Production, explains how stablecoins, real-time settlement and embedded compliance improve UX, risk controls and reporting across banking and payments platforms. Learn where AI and data pipelines create measurable gains in cost, speed and governance and what to build next.

Key Takeaways: FinTech trends 2026 for CTOs, product leaders and system architects 4

These key takeaways summarize what FinTech teams must design, implement and validate in production in 2026. From hybrid finance architectures and real-world asset tokenization to AI-driven transaction agents and privacy-preserving compliance.

- Hybrid Finance Architecture Hybrid finance platforms in 2026 combine off-chain data processing for performance with on-chain settlement and auditability, allowing banks and FinTech companies to scale payments without sacrificing compliance.

- RWA Tokenization & Custody RWA tokenization enables institutional-grade liquidity for bonds and real estate, with MPC custody and forced transferability becoming mandatory standards for regulated tokenized asset platforms.

- Zero-Knowledge Identity (ZK-ID) Zero-knowledge identity allows regulated financial institutions to meet KYC and AML requirements while minimizing data exposure, reducing compliance risk and operational liability.

- AI-Driven Financial Agents AI-driven financial agents automate payments, rebalancing and compliance workflows autonomously, with every on-chain action validated by policy and risk models before settlement.

Introduction: The rapid evolution of FinTech and AI agents

The FinTech industry stands at an inflection point. As we navigate through this decade, the global FinTech landscape in 2026 is being reshaped by accelerating new trends in FinTech, surging investment and new regulatory frameworks. It is no longer just a buzzword or a challenger ecosystem. FinTech is booming and there is no stopping it. For enterprise leaders and software architects alike, now is the time for the FinTech industry, a transformation of the financial industry that demands a fundamental rethink of how we process value. Since we passed January 2025, the pace has only quickened, driven by substantial funding and FinTech innovations. The sheer scale of the market validates this significant shift, reshaping how industries operate. Today, there are north of 26,000 FinTech start-ups globally, more than double the number five years ago. However, quantity does not equate to quality. In my 23 years of architecting enterprise-grade systems, I have seen waves of hype come and go, with data points from 2022 and 2023 serving as learning curves, but this era is different. The difference in 2026 is that we are moving from experimental pilots to the critical digital infrastructure of financial institutions, impacting every vertical from the neobanking to manufacturing and insurance. We are no longer just building apps. We are re-architecting the global financial nervous system to deliver better outcomes and financial products for people around the world. This transformation could be the most important product structural change of our time and every company must adapt to survive. The FinTech market is expected to mature significantly, making financial services and core banking infrastructure more efficient.

What Drives Global FinTech Trends in 2026?

How Global Dynamics Shape FinTech Diversification

Before we dive into the deep technical architecture, it is crucial to understand the breadth of this transformation. Market context: what shapes FinTech patterns is often a mix of consumer demand and institutional necessity. It is also geographically nuanced. Across major regions, FinTech emerging trends are playing out differently. For instance, in North America, we see a heavy focus on institutional custody. Meanwhile, mobile money and emerging FinTech are booming in places like India, which continues to lead in real-time cashless payments via phone-based interfaces. Not a cash anymore. Major analysts highlight that the convergence of services into super apps is driving user expectations for seamless interoperability across different countries. This defines FinTech services in 2026. Reflecting on the industry, here are some of the biggest media news highlights focused on specific companies and shifts within the FinTech sector. Diversification is everywhere. We see massive innovations ranging from the top 9 digital payment trends to keep an eye on in 2026—such as biometric checkout and stablecoin rail to niche verticals like the top ticketing industry innovations to keep an eye on in 2026, where NFT-based ticketing is eliminating fraud. This content is becoming increasingly relevant as firms expand their operations to meet rising user demands. If you read this blog article, you will see how leading players stay relevant to these changes. Furthermore, looking back at 2025 shifts, we see that specific sectors were projected to reach over a billion in 2025.

How to Move From FinTech Predictions to Architecture

While the web is flooded with speculative articles and generic trend lists for 2026, growing companies cannot afford to build their strategy on hype. As an architect, I filter out the noise to focus solely on the actionable engineering trends shaping global banking. We are moving past the 2024-2025 experimental phase directly into critical infrastructure upgrades. Now, let’s review what drives these FinTech movements and explore each one in detail. We will examine emerging technologies transforming FinTech and trends: highlights. This guide breaks down the top trends and what to expect in 2026. So here are what I believe will be the significant trends impacting banking, financial services, banks and FinTech in 2026. While lists vary—some cite what’s next in finance: top 6 FinTech shifts for 2026 or the six FinTech directions shaping 2026—the following architectural shifts are the absolute foundation for any CTO building for the future. These shifts are shaping the future of global banking and digital banks.

The rise of hybrid embedded finance: Merging real-time on-chain transparency with off-chain scalability

In my two decades as a dApps architect, I have watched the financial sector swing like a pendulum between rigid centralization and chaotic decentralization. For years, the narrative was binary: either you stuck with legacy platforms that were secure but slow, or you went full Web3, which offered transparency but struggled under the weight of enterprise-grade volume. Entering 2026, that binary choice is dead. We are witnessing the maturation of an architecture that leverages the best of both worlds, providing a solution that helps firms grow well beyond their initial projections. In this way, it bridges the gap between traditional financial institutions and decentralized protocols and services. This is what we call Hybrid Finance, a structural change where high-frequency trading and sensitive customer data remain off-chain for speed and privacy, while settlement, reconciliation and audit trails move on-chain for immutability. This is not just a theoretical upgrade. It is a survival plan. The FinTech sector is growing rapidly, with revenues forecast to hit $1.5 trillion by the end of the decade, according to Boston Consulting Group. To capture a slice of that valuation, financial institutions must abandon the idea that financial blockchain is an experimental sandbox and start treating it as a production-grade backend component. FinTech adoption provides a significant competitive advantage in a crowded marketplace, shaping business policy. This is reshaping the latest FinTech trends 2026.

The data behind the shift: FinTech market trends after 2025

The urgency to adopt these models is driven by the sector’s rapid pace. With an anticipated compound annual growth rate of 20.3%, the FinTech sector is expected to reach $698.5 billion by 2030. To understand the magnitude, we must analyze global FinTech size, growth & investment trajectories. Reviewing 2025 trends: market share & statistics helps clarify why raw growth is meaningless if your infrastructure collapses under the load.

📊 Pharos Production Internal Benchmark: 2025 Performance

While external reports highlight market growth, our direct engineering data reveals the operational impact. Metrics aggregated across multiple regulated environments using comparable transaction volumes and settlement profiles. Across 12 enterprise migrations to Hybrid Architecture executed by our team in 2025, we observed the following average efficiency gains compared to legacy setups:

Source: Pharos Production Anonymized Client Data, Q4 2025

The winners are those building bridges. They are integrating decentralized finance protocols and services into their existing stacks to address specific pain points, such as liquidity fragmentation and slow cross-border settlement. This is one of the top 5 FinTech developments shaping the financial industry today. When we architect these platforms, we look for the “golden mean”. Using SQL databases for user profiles and session management to ensure a snappy customer experience, while anchoring transaction hashes to a distributed ledger for undeniable proof of settlement. This collaboration between banks and digital FinTech is crucial for long-term stability.

Real-time payments (RTP) ecosystem and cross-border efficiency landscape in 2026

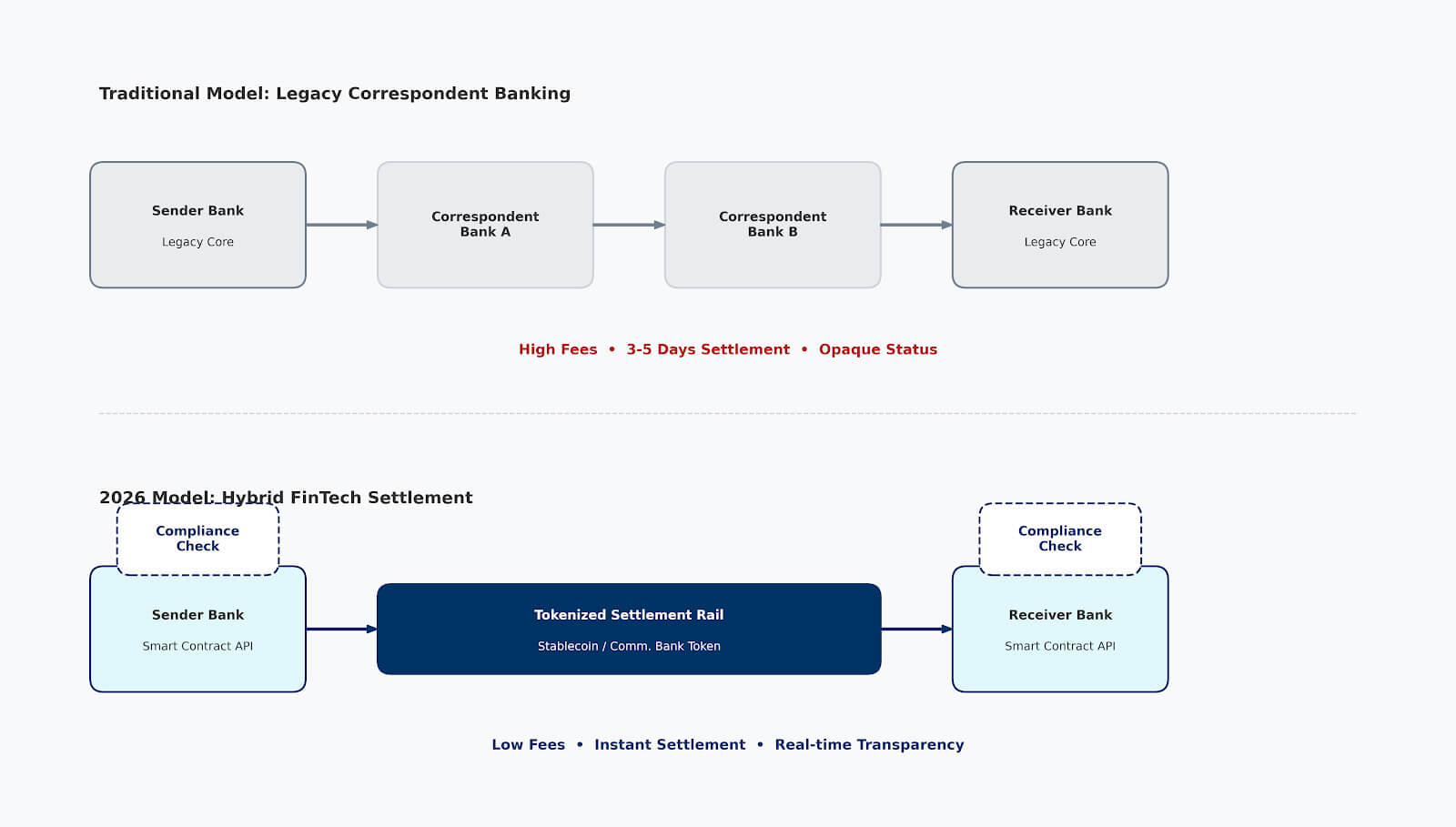

Nothing exposes the limitations of purely traditional banking quite like cross-border payments. To understand why Hybrid Finance is the architectural choice for 2026, we must compare the settlement models directly:

| Feature | Traditional Correspondent Banking | Hybrid Finance (Stablecoins/CBDC) |

|---|---|---|

| Speed | Days (T+2 or T+3) | Instant (Real-Time Settlement) |

| Transparency | Opaque (Black box intermediaries) | Transparent (Shared Ledger) |

| Liquidity | Trapped in pre-funding accounts | Freed capital (Atomic Swaps) |

| Compliance | Manual / Siloed checks | Embedded (Smart Contract Logic) |

This allows real-time payments to settle instantly, rather than just appear to settle while the back office catches up three days later. For a CTO, this changes the risk profile entirely. Instead of reconciling databases between five different financial institutions, we have a shared source of truth. This reduces operational overhead and frees up capital that was previously locked in pre-funding accounts. This efficiency is why a central bank digital currency (CBDC) and specific projects like the European Central Bank’s digital euro (EU) are gaining such massive traction. They are the fuel for these engines, optimized logistics and supply chains. This modernization makes the process easier for consumers and providers alike, enabling the instant processing of millions of transactions year over year. The adoption of such innovative FinTech platforms is a part of FinTech funding strategies for the coming years.

This allows real-time payments to settle instantly, rather than just appear to settle while the back office catches up three days later. For a CTO, this changes the risk profile entirely. Instead of reconciling databases between five different financial institutions, we have a shared source of truth. This reduces operational overhead and frees up capital that was previously locked in pre-funding accounts. This efficiency is why a central bank digital currency (CBDC) and specific projects like the European Central Bank’s digital euro (EU) are gaining such massive traction. They are the fuel for these engines, optimized logistics and supply chains. This modernization makes the process easier for consumers and providers alike, enabling the instant processing of millions of transactions year over year. The adoption of such innovative FinTech platforms is a part of FinTech funding strategies for the coming years.

What most FinTech companies don’t understand about FinTech sector trends 2026

There is a dangerous misconception I often encounter in boardrooms regarding legacy modernization:

We build these “adapters” to allow a 30-year-old banking system to interact with a smart contract as if it were just another API endpoint. We build these “adapters” to allow a 30-year-old banking system to interact with a smart contract as if it were just another API endpoint. This methodology mitigates risk and lowers the barrier to entry. It allows financial institutions to offer their customers yields from decentralized finance or tokenized assets through a familiar, regulated interface. By merging on-chain transparency with off-chain scalability, we are not just making environments faster. We are enabling them to scale. We are making them more honest without sacrificing the performance users demand. It is time to think about how to combine these tools to enhance your offering, using reporting capabilities to create information already expanding online. This reflects the digital growth in 2026.

Technical architecture of financial service: How to integrate DeFi protocols into enterprise banking systems using artificial intelligence

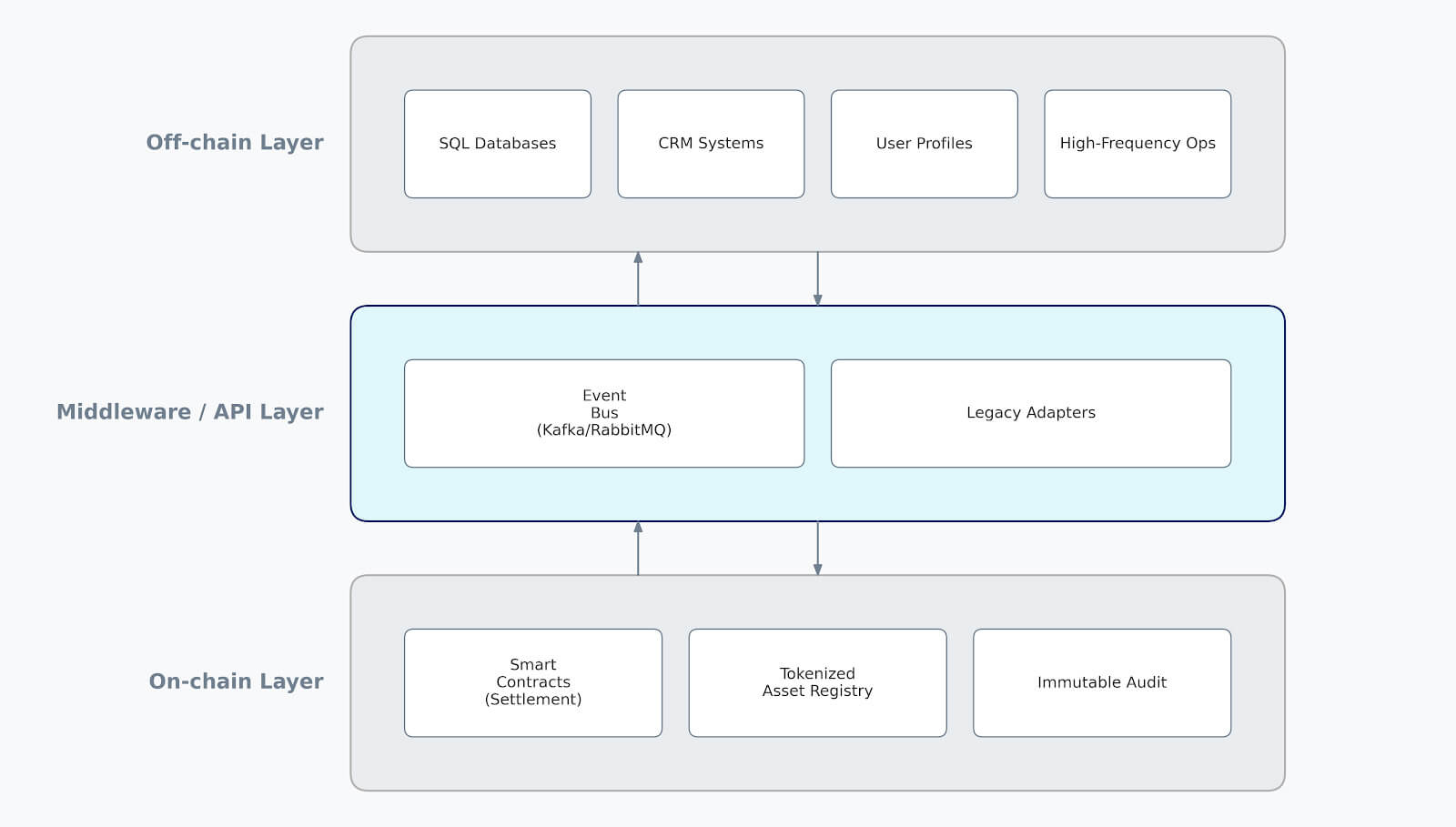

In 2026, artificial intelligence in FinTech is no longer just about offering new FinTech products. It’s about rethinking infrastructure, workflows and experiences from the ground up. As a dApps architect who has spent decades dismantling and rebuilding financial engines, I can tell you that integrating Decentralized Finance (DeFi) protocols and services into enterprise environments is one of the intellectually demanding challenges in our field. It is not merely a matter of connecting an API. It is about reconciling two fundamentally different states of truth. You have the probabilistic finality of a financial blockchain collision with the deterministic finality of a legacy SQL database. Bridging this gap requires a sophisticated high-load backend middleware that handles state management, nonce synchronization and gas fee estimation without the end-user ever knowing a financial blockchain is involved.

Across multiple regulated FinTech and banking projects, a clear architectural pattern emerges. We build event-driven architectures of smart contracts that act as the settlement engine, while the traditional core serves as the system of record for customer data. This methodology prevents the “garbage in, garbage out” problem by ensuring that data validated by predictive analytics models off-chain is the only data that ever triggers an on-chain transaction. This is the bedrock of modern solutions enabled by new financial protocols. FinTechs are using these methods to ensure robustness.

Across multiple regulated FinTech and banking projects, a clear architectural pattern emerges. We build event-driven architectures of smart contracts that act as the settlement engine, while the traditional core serves as the system of record for customer data. This methodology prevents the “garbage in, garbage out” problem by ensuring that data validated by predictive analytics models off-chain is the only data that ever triggers an on-chain transaction. This is the bedrock of modern solutions enabled by new financial protocols. FinTechs are using these methods to ensure robustness.

Top trends in embedded finance and the API connectivity layer

The concept of embedded finance has evolved significantly. It is no longer just a retailer offering a “Buy Now, Pay Later” (BNPL) button. It represents a diverse ecosystem: how FinTech extends beyond payments into insurtech, wealth management, peer-to-peer lending and alternative credit models directly within non-financial platforms. To achieve this technically, we rely heavily on open banking APIs and Banking-as-a-Service infrastructure. These APIs act as a translation layer, enabling SaaS platforms to seamlessly integrate financial services. They take a complex DeFi yield farming operation and abstract it into a simple RESTful endpoint, which is seamlessly consumable by native iOS and Android financial apps. This ensures that data can be queried by any unified cross-platform interface without latency. This helps businesses manage processes and loans, thereby increasing opportunities for small retail players. This transformation marks the era of B2B FinTech, in which every interaction is a payment. For an enterprise banking system, the architecture must support high throughput. We often implement a queuing system, such as Kafka or RabbitMQ, between the bank’s internal ledger and the public nodes. This buffer is critical for payments for services. It allows the bank to operate at thousands of operations per second and the financial blockchain settles batches asynchronously. This decoupling ensures that user experience remains snappy, even if the underlying network is congested. It is a pragmatic application of FinTech development patterns 2026, focusing on resilience over raw decentralization.

The convergence of AI agents and generative AI

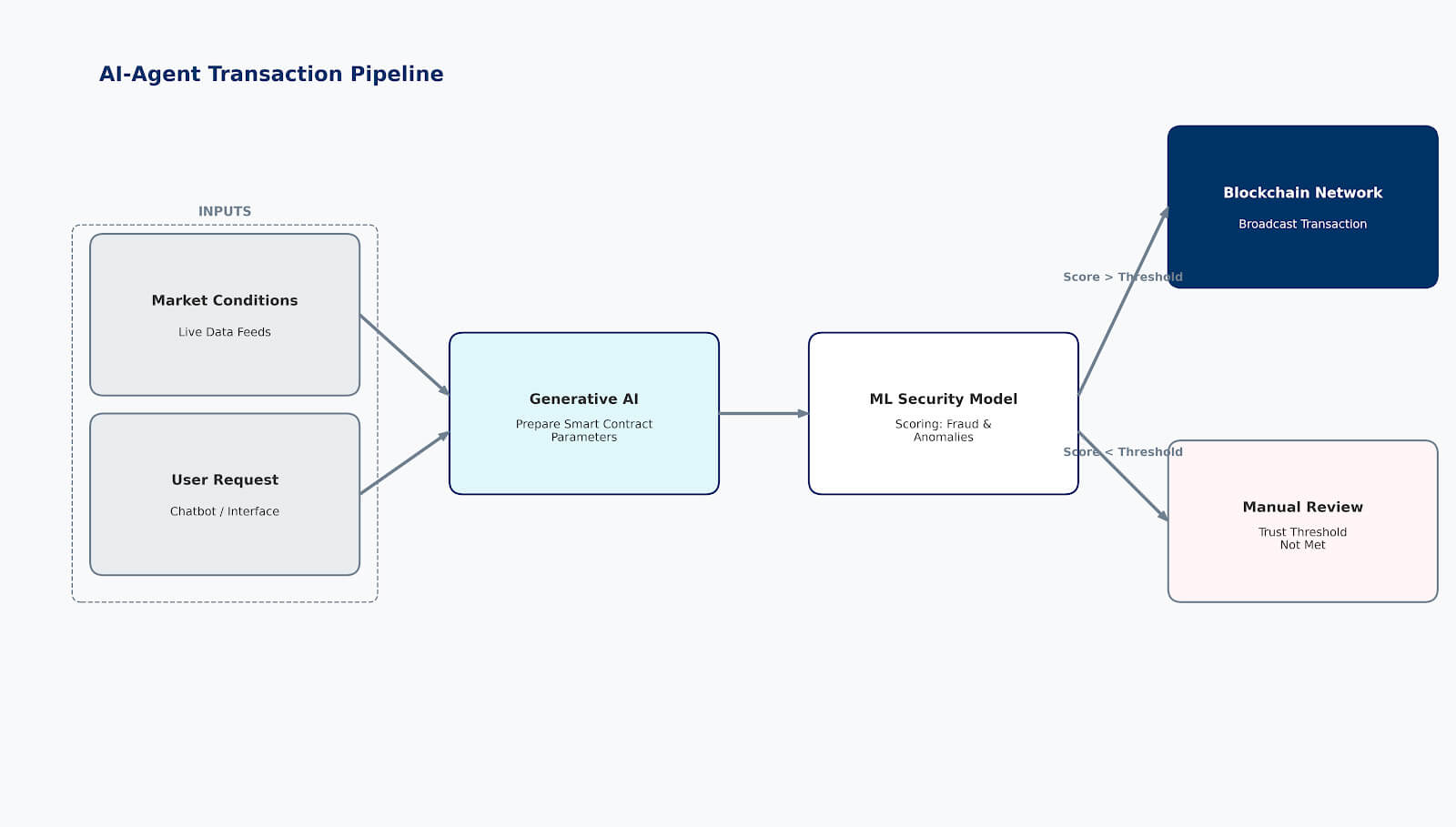

2026 Transaction Security Pipeline

Generates strategy and drafts the smart contract transaction based on market data.

Scores transaction for anomaly detection and fraud risk (0-100 Score).

If Score > Threshold, the transaction is broadcast. If it fails, it is flagged for human review.

One of the transformative shifts we are witnessing is the role of autonomous AI models. We are moving from static scripts to dynamic AI agents and AI-powered chatbots that can execute complex financial strategies using advanced natural language processing. In this architecture, generative AI plays a surprising role. It is not just generating text. It is used to write and verify lightweight smart contract interactions on the fly, tailored to specific customer needs. These AI agents can monitor market conditions and execute trades or rebalance portfolios without human intervention, while strictly adhering to the risk parameters defined by the user. This is a prime example of AI and machine learning in action.  However, granting autonomy to code requires rigorous guardrails. We integrate machine learning models directly into the transaction pipeline to deliver personalized services that drive deep customer engagement. Before an AI agent broadcasts a transaction to the financial blockchain, a separate ML model scores the transaction for anomaly detection and fraud risk. If the score passes the threshold, the transaction proceeds. If not, it is flagged for manual review. This dual-layer path allows financial institutions to leverage the speed of automation while maintaining the safety nets required by rules and regulations. Personalization is coming, reshaping wallets and e-commerce with unique recommendations tailored to customer needs. We can automate these areas to ensure accuracy. The role of AI in FinTech is becoming central to compliance. In fact, FinTech companies are using AI tools to detect fraud. This represents a massive shift in AI adoption.

However, granting autonomy to code requires rigorous guardrails. We integrate machine learning models directly into the transaction pipeline to deliver personalized services that drive deep customer engagement. Before an AI agent broadcasts a transaction to the financial blockchain, a separate ML model scores the transaction for anomaly detection and fraud risk. If the score passes the threshold, the transaction proceeds. If not, it is flagged for manual review. This dual-layer path allows financial institutions to leverage the speed of automation while maintaining the safety nets required by rules and regulations. Personalization is coming, reshaping wallets and e-commerce with unique recommendations tailored to customer needs. We can automate these areas to ensure accuracy. The role of AI in FinTech is becoming central to compliance. In fact, FinTech companies are using AI tools to detect fraud. This represents a massive shift in AI adoption.

FinTech development: Reconciling Smart Contracts with legacy systems

The friction point for CTOs is the rigidity of legacies. Mainframes built in the 1990s were never designed to listen to an Ethereum event log. To solve this, we implement “Oracle” services that function in reverse. Instead of just feeding off-chain data into the blockchain, these services listen for on-chain events, such as a completed loan repayment and push that state change back into the legacy core. This bidirectional flow ensures that the bank’s balance sheet is always in sync with the distributed ledger. This integration provides a level of transparency previously impossible. When a smart contract executes a payout, the audit trail is generated instantly. There is no need to wait for a nightly batch job to process the day’s files. For our enterprise clients, this real-time reconciliation is the primary driver for adoption, turning what used to be a back-office nightmare into a streamlined, automated process. We see several increased benefits in integrated center studies.

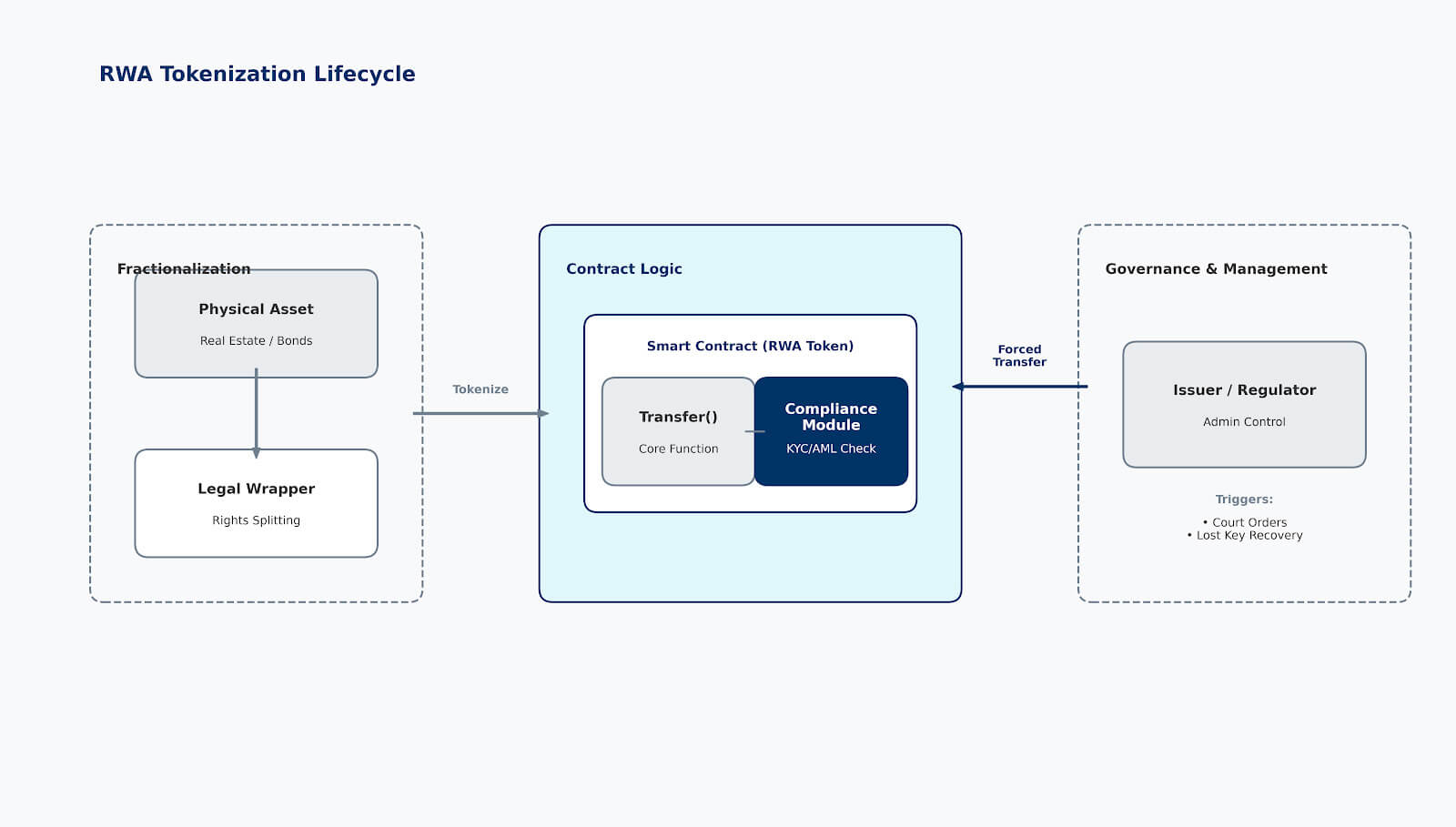

Real-world asset tokenization trends shaping standards and infrastructure for institutional adoption

For years, the promise of moving physical value onto a digital ledger was discussed in the future tense. In 2026, we have moved firmly into the execution phase. Tokenized real-world assets represent the single largest opportunity for financial institutions to unlock liquidity in illiquid markets. We are no longer talking about speculative JPEGs. We are talking about commercial real estate, government bonds and private equity funds being fractionalized and traded 24/7. Yet – whether they know it or not – blockchain remains a FinTech force because it solves the fundamental problem of settlement latency in these high-volume markets. It provides a clear advantage. These are real-world FinTech innovation examples. At Pharos Production, we see a distinct shift in how our enterprise clients approach this. They are no longer asking “what is a token?”. They are asking “how do we custody it safely?” and “which standard supports forced transfers for legal compliance?” This maturity signals that asset tokenization has graduated from a sandbox experiment to a core business framework. Real-world innovation examples are now visible in major treasury departments. Short-term government debt is being tokenized to serve as on-chain collateral, creating a capital efficiency cycle that was impossible with paper-based certificates. It is changing times for mainstream adoption. This is defining the landscape in 2026.

Infrastructure and the digital wallet evolution: Key trends

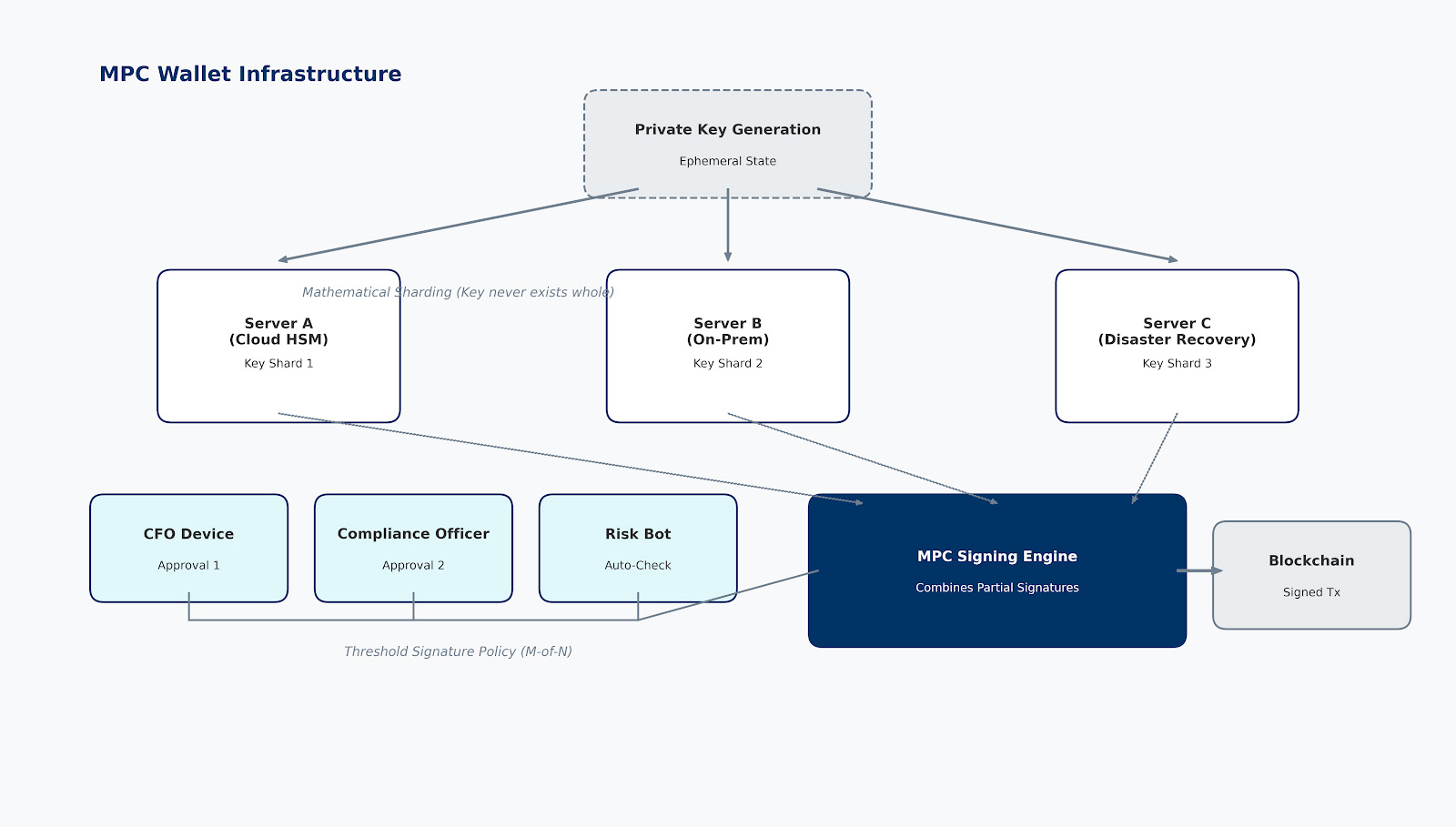

The gateway to this new economy is the digital wallet, but the technology powering it has changed drastically. Institutional investors cannot rely on a browser extension. We are building infrastructure based on MPC:

Multi-Party Computation (MPC)

Definition: A cryptographic security model where a private key is never generated in a single location. Instead, it is “shattered” into mathematical shards and distributed across different servers and devices.

This growth in the crypto wallet finally gave compliance officers the confidence to sign off on blockchain pilots.  This growth in the crypto wallet finally gave compliance officers the confidence to sign off on financial blockchain pilots. It allows for granular governance policies. For example, requiring approval from the CFO, an officer and an automated risk bot before any funds over $100,000 can leave the wallet. This infrastructure is the backbone of institutional adoption. It turns a “bearer asset” instrument, which is terrifying for a bank, into a programmable financial instrument with built-in checks and balances. This enables large firms to invest total revenue in new programs with confidence, while keeping track of spending. You handle your own keys, ensuring your assets are safe.

This growth in the crypto wallet finally gave compliance officers the confidence to sign off on financial blockchain pilots. It allows for granular governance policies. For example, requiring approval from the CFO, an officer and an automated risk bot before any funds over $100,000 can leave the wallet. This infrastructure is the backbone of institutional adoption. It turns a “bearer asset” instrument, which is terrifying for a bank, into a programmable financial instrument with built-in checks and balances. This enables large firms to invest total revenue in new programs with confidence, while keeping track of spending. You handle your own keys, ensuring your assets are safe.

Blockchain standards and compliance logic for FinTech solutions

When we architect these platforms, the choice of token standard is critical. You cannot simply use a basic ERC-20 token for a security. It lacks the necessary control. We utilize standards that support permissioned transfers, ensuring that a token can only be sent to a wallet that has passed Know Your Customer and Anti-Money Laundering checks. This logic is baked directly into the smart contract. If a wallet tries to send a tokenized share of a building to a non-whitelisted address, the operation reverts automatically. The code enforces the regulation.  This level of control is essential for the innovation of FinTech services for banks in regulated markets. It allows issuers to maintain a “clean” cap table automatically, without manual reconciliation. Furthermore, it enables features like automated dividend distribution. A smart contract can payout stablecoins to thousands of token holders in a single block. This significantly reduces administrative costs and enhances the investment appeal of previously cumbersome asset classes. It offers multiple options for investing in a diversified portfolio of tokenized assets, allowing optional edge cases to be easily handled via their own governance modules. FinTech platforms and services are now integrating these banking standards by default.

This level of control is essential for the innovation of FinTech services for banks in regulated markets. It allows issuers to maintain a “clean” cap table automatically, without manual reconciliation. Furthermore, it enables features like automated dividend distribution. A smart contract can payout stablecoins to thousands of token holders in a single block. This significantly reduces administrative costs and enhances the investment appeal of previously cumbersome asset classes. It offers multiple options for investing in a diversified portfolio of tokenized assets, allowing optional edge cases to be easily handled via their own governance modules. FinTech platforms and services are now integrating these banking standards by default.

Using standard ERC-20 tokens for Real-World Assets.

Standard tokens are “bearer assets.” If keys are lost or stolen, the asset is gone. This fails regulatory requirements.

Implementing “Forced Transfer” Extensions (ERC-1400/ERC-3643).

Allows the issuer to burn lost tokens and re-mint them to a new wallet, satisfying legal court orders and recovery protocols.

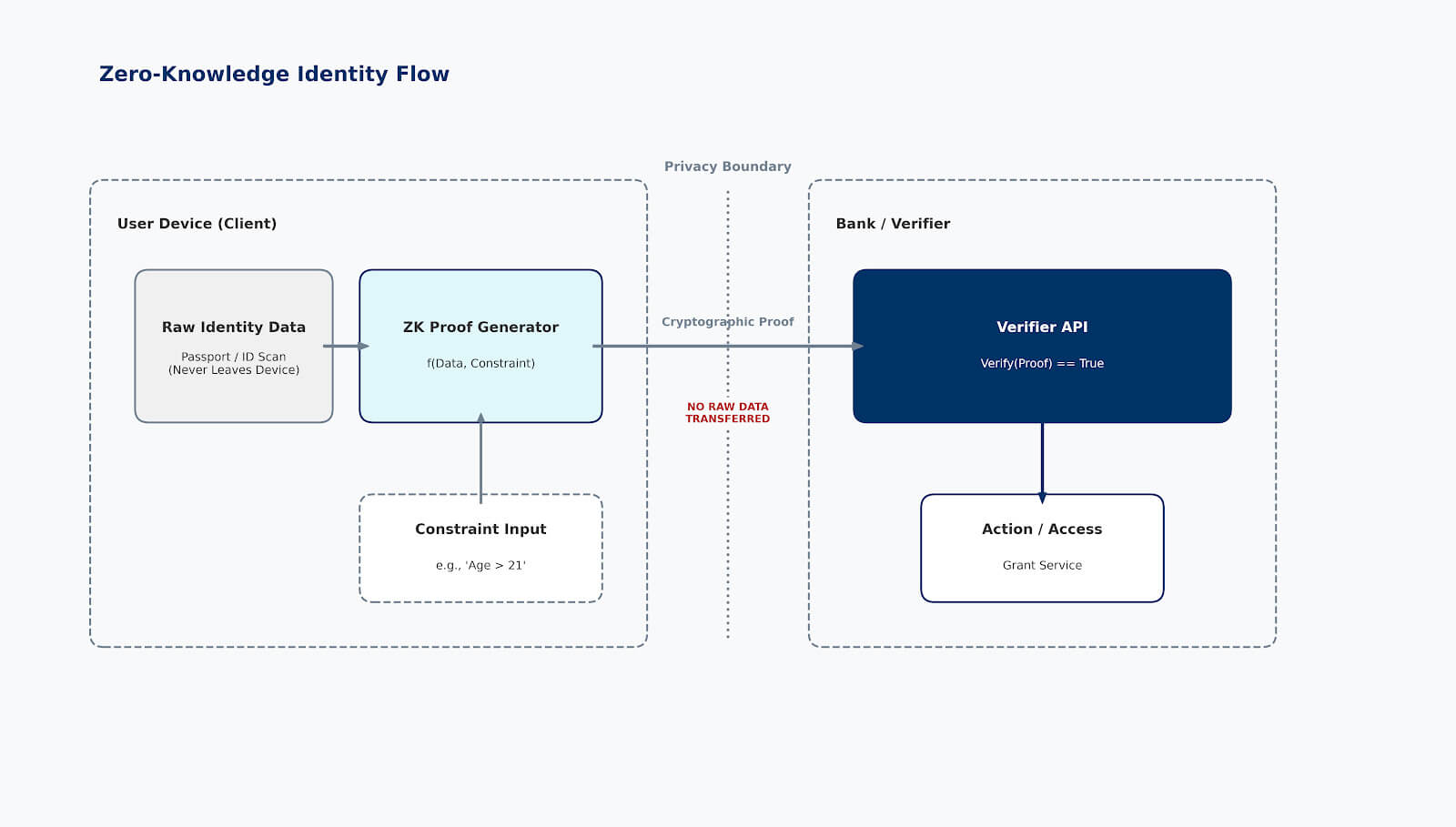

Security and compliance 2026: Implementing zero-knowledge identity in regulated global FinTech markets and decentralized finance

As we look ahead, four FinTech inclinations stand out and are set to shape the landscape in 2026, from an operational and a risk-and-fraud prevention perspective. Among these four major FinTech currents for 2026, we see Zero-Knowledge Identity, detection of synthetic identities, AI-driven surveillance and the mandatory enforcement of operational resilience. In my role at Pharos Production, I have seen the conversation shift dramatically. Security architecture is no longer just about installing a firewall. It is a dynamic architecture that must protect personal privacy, simultaneously satisfying the most aggressive regulatory requirements we have ever seen. The defining challenge for the modern CTO is the paradox of data. To prevent fraud, financial establishments historically hoarded massive amounts of sensitive customer data, passports, tax returns and biometric markers. However, in 2026, holding this data is a liability, not an asset. Every record stored is a potential leak vector, especially given the looming threat of quantum computing, which can break current encryption standards. This is why we are aggressively pivoting toward Zero-Knowledge Proofs. This cryptographic breakthrough allows a user to prove a statement is true, such as “I am over 21” or “I am a chaotic accredited investor”, without revealing the underlying evidence. We verify the fact, not the document, streamlining the verification process.

Core Definition

Zero-Knowledge Proof (ZKP)

A cryptographic method that allows one party (the prover) to prove to another party (the verifier) that a statement is true, without revealing any information beyond the validity of the statement itself.

The evolution of compliance: Zero-knowledge proofs are the future of FinTech

Implementing ZK-based identity environments changes the fundamental logic of KYC and Anti-Money Laundering (AML) workflows. In a traditional setup, a person uploads their ID to a server where it sits encrypted at rest, hopefully safe. In a ZK architecture, the person generates a cryptographic proof locally on their device. The bank verifies this proof on-chain or via a secure API. The bank never sees the raw ID, yet regulatory compliance is fully satisfied because the proof is mathematically irrefutable. This is the holy grail of data privacy in services.  In this way significantly reduces the attack surface for cybercriminals. If a database contains only cryptographic proofs rather than raw identity data, it is worthless to a hacker. This shift is also driving sustainable, ESG-focused FinTech, specifically within the “Governance” services pillar. By minimizing data retention, companies reduce their digital carbon footprint and their legal liability, creating a leaner, more responsible corporate structure that aligns with global privacy standards and green sustainability initiatives. This optional layer of security is becoming mainstream, particularly as ESG becomes a strong metric. We use this to detect issues in the same way modern protocols do. This is a core component of green FinTech services.

In this way significantly reduces the attack surface for cybercriminals. If a database contains only cryptographic proofs rather than raw identity data, it is worthless to a hacker. This shift is also driving sustainable, ESG-focused FinTech, specifically within the “Governance” services pillar. By minimizing data retention, companies reduce their digital carbon footprint and their legal liability, creating a leaner, more responsible corporate structure that aligns with global privacy standards and green sustainability initiatives. This optional layer of security is becoming mainstream, particularly as ESG becomes a strong metric. We use this to detect issues in the same way modern protocols do. This is a core component of green FinTech services.

FinTech industry trends in regulatory technology

The digital regulatory environment has become incredibly complex with the maturation of frameworks like DORA in Europe and similar mandates in the US, alongside increasing oversight from the Consumer Financial Protection Bureau. Regulators are no longer satisfied with passive compliance. They demand active, real-time proof of resilience. This has led to “RegTech” becoming a critical layer in our engineering stack. We now build platforms where compliance logic is embedded directly in the code. If a transaction violates a sanction list, it is not flagged for later review. It is blocked at the protocol level. We must track changes quickly to identify risks. We are also seeing a convergence of digital fraud prevention and financial transparency enabled by blockchain payments. By utilizing public ledgers for transaction monitoring, we can spot money laundering patterns across financial institutions without sharing sensitive client lists. This shared intelligence network allows banks to be proactive rather than reactive, stopping bad actors before they can exit the ecosystem. It is a collaborative way to cybersecurity that was impossible in the siloed world of Web2. We must continue monitoring AI in the FinTech market services for new threats.

Enhancing customer experience through invisible security at financial institutions after 2024

The historical trade-off has always been that greater security comes at the cost of a worse user experience. We all hate 2FA codes and endlessCAPTCHAs. However, the goal of modern architecture is to ensure the security of bank services that remain invisible. By leveraging biometric recognition and ZKPs, we can authenticate users with a single face scan that generates a proof, eliminating passwords entirely. This directly improves people’s experience, reducing drop-off rates during onboarding while actually increasing the level of assurance and accuracy. When we design these products, we focus on “frictionless trust.” The client should feel safe without feeling burdened. For example, instead of freezing an account when a client travels, our AI agents analyze behavioral biometrics and device telemetry in real time to seamlessly authorize access. This is what the standard users expect in 2026. They want their financial apps to be as secure as a vault but as easy to use as a social media feed. It brings the bank’s power right to their home, detecting threats in the same way a physical guard would. This tailored approach is the only way forward.

Reshape from legacy to Web3 and open banking: A step-by-step migration strategy for FinTech industry leaders

We have explored the architecture, the regulatory landscape and the specific digital technology defining 2026. Now, we arrive at the most critical juncture: execution. Developing a robust strategy for companies entering 2026 requires a calculated migration strategy, not a reckless leap. I have overseen enough digital transformations to know that the “big bang” approach, switching everything overnight, is a recipe for disaster. Instead, successful migration requires a phased, parallel adoption model. Segments reshaping finance show that gradual integration yields higher stability. Evolving FinTech products demand this patience. Developing a robust strategy for companies entering 2026 requires a calculated migration strategy. Here is the 3-step phased adoption model we implement:

Decoupling & Microservices

Break down monolithic legacy applications. Move from hard-coded internal calls to cloud-native microservices to prepare data structures for distributed systems.

API Connectivity

Ensure core banking functions interact via APIs. This creates the “translation layer” required for legacy systems to speak with external blockchain networks.

Hybrid State Implementation

Swap specific modules. Keep the UI on standard cloud servers, but move the settlement engine to a private blockchain to test stability without risking the enterprise.

The Human Element in FinTech Strategy

Technology is often the easy part. The cultural shift is where the friction occurs. The challenge lies in bridging the skills gap. You can buy the best software, but without humans to implement these digital technological solutions, the leaps in efficiency and growth that FinTech will provide for financial services will remain a pipe dream. Your existing team of COBOL or Java developers needs to understand the nuances of Solidity, Rust, or Zero-Knowledge architecture. This requires a dedicated investment in training or augmenting your staff with an expert team that has lived through these cycles before, often requiring a deep understanding of data science to analyze on-chain patterns. This enables broader participation early on, fostering career success within your org. We see this AI adoption across teams. The administrative side of transformation is equally daunting. CTOs often find themselves analyzing the cost breakdown of a FinTech app and its services, or vetting developers to augment their internal squads. Generalist FinTech consulting services and even FinTech marketing agencies play a role in the ecosystem. The core engineering challenge demands deep, specialized architectural oversight. You need to check your resources and view these decisions as opportunities for partnerships and getting well ahead of the curve. For FinTech startups, the challenge is different. They often have the technical agility but lack the institutional knowledge to navigate scale. They need to balance rapid innovation with the stability required by banks they hope to partner with. This is where mentorship and strategic hiring become more valuable than venture capital. You need architects who understand both the anarchy of cryptocurrencies and the rigidity of the Federal Reserve. This is the way to improve the startup ecosystem. New movements in services favor those who prepare.

Engineering Capabilities Required to Build These FinTech Systems

These capabilities are typically delivered by teams experienced in building regulated FinTech platforms, hybrid blockchain architectures and AI-driven systems. This brings me to a crucial realization for any CTO. You cannot build the future entirely in-house. The pace of change in FinTech motions for 2025 and 2026 is simply too fast to master every vertical internally. This is why you need the right FinTech provider: introducing Pharos Production. With 23 years of experience in digital product development, we specialize in bridging these two worlds. We do not just write code. We architect solutions that survive audits and scale under pressure. You can learn more about our innovative case studies and expertise on our web platform. Keeping up with the latest FinTech directions ensures we stay ahead, including AI. Our approach to custom soft is deeply rooted in the reality of your business. Whether you are looking for high-level blockchain development or complex Web3 and AI integrations, we provide architectural oversight to prevent costly mistakes. We act as the technical co-pilot, helping you navigate the transition from legacy infrastructure to future-proof infrastructures. We understand that development is not a commodity. It is the central nervous system of your organization. FinTech companies that adapt and lead will thrive in this emerging market.

Global FinTech trends in 2026 and beyond

As we close this exploration, remember that the landscape will continue to shift. The FinTech paths we discussed for 2026. Hybrid finance, RWA tokenization and ZK-identity, AI and ML are just the beginning. The game-changing patterns that will separate leaders from those left behind are often invisible to the end user but foundational to the business. FinTech companies that adapt and lead will thrive in this emerging market, while those that cling to the safety of pure legacy infrastructure will find their margins eroded by more efficient competitors. The goal is not to use blockchain payments for its own sake, but to build a digital financial system that is more transparent, efficient and accessible. Still, further benefits will continue to emerge in the last months of the year, providing new ways to handle value exchange. Getting well prepared is the best policy. This is the future of FinTech movements in 2026.

Final notes on top FinTech trends

If you are ready to take the next step in your migration journey, or if you need an audit of your current architecture to determine where Web3 and AI fit, my team and I are ready to help. We are builders at heart and passionate about building the next generation of financial infrastructure. Explore our FinTech report’s latest findings, insights and market analysis to uncover strategies driving financial technology. For more information, or to contact our team, email us or check our terms and policy. The contents of this article are for information purposes. All rights reserved. Watch for indicators in 2026.

Frequently Asked Questions (FAQ)

Navigate the technical nuances of FinTech 2026. From the architecture of Hybrid Finance to the implementation of Zero-Knowledge Identity, these answers provide the engineering context needed for decision-making in the post-2025 landscape.

Type to filter questions and answers. Use Topic to narrow the list.

Showing all 11

No matches

Try a different keyword, change the topic, or clear filters

-

Hybrid Finance in 2026 is an architecture that keeps product UX and most app data in Web2 systems while anchoring settlement and audit events on-chain. Choose it when you need low latency user experiences and verifiable settlement across multiple parties with programmable rules.

The main limitations are regulatory and operational complexity around custody and key management plus reconciliation risks and chain cost or latency spikes.

Key points- Keep UX and most data in Web2, anchor settlement and audits on-chain

- Choose it for low latency and verifiable multi-party settlement with programmable rules

Learn more: Hybrid Finance 2026 Opens in the same page.

-

ZK-Identity is a compliance approach where users prove KYC and eligibility claims with zero-knowledge proofs instead of sharing raw documents. Use it when your priority is data minimization and selective disclosure while keeping verification portable and audit-ready.

The constraints are trusted credential issuers and revocation and dispute processes plus proof system complexity and integration overhead.

Key points- Prove eligibility and KYC claims with zero-knowledge proofs, not raw documents

- Use it to reduce data exposure and enable portable verification across partners

Reference: ZK Identity Banking Compliance

-

RWA tokenization is the representation of real-world assets as regulated on-chain tokens so ownership and transfers can be automated and audited. It is most useful when you want fractional access and faster delivery versus payment and programmable corporate actions for assets with clear legal wrappers.

The hard parts are legal structuring and custody and identity gating and reliable pricing and corporate action data rather than the token contract itself.

Key points- Tokenize real-world assets to make ownership programmable and settlement faster and auditable

- Works best when compliance rules and transfer restrictions must be enforced automatically

Reference: RWA Tokenization

-

AI agents in FinTech are software actors that execute workflows by calling APIs and proposing or triggering financial transactions. Plan for them when you want automation across operations and customer support and treasury and you can enforce policies and approvals and monitoring around every action.

Without guardrails they can generate unsafe transactions or leak sensitive data or create compliance violations so production needs strict limits and simulation and anomaly detection and an auditable control plane.

Key points- Agents shift systems to tool-driven workflows with policy checks and audit trails

- You need scoped credentials, approvals and observability, not direct unattended signing

Reference: AI Agents FinTech Infrastructure

-

A stablecoin rail is a payments and settlement path where value moves via stablecoin transfers rather than traditional interbank messaging and settlement. It makes sense for high frequency cross-border flows and treasury rebalancing and programmable settlement when you have reliable liquidity and on and off ramps and compliance monitoring.

The key risks are issuer and depeg exposure and regulatory uncertainty and dependency on custodians and exchanges plus chain outages or fee volatility.

Key points- Stablecoin rails enable 24/7 settlement for payments, treasury and cross-border transfers

- Use them when bank cutoffs hurt and API-native settlement improves operations

Reference: Stablecoin Rails

-

Off-chain components are databases and services for personal data and analytics and high frequency reads and writes while on-chain components hold settlement-critical state and issuance and shared audit events. Put functionality on-chain when it must be independently verifiable across parties or deterministically executable under agreed rules and keep it off-chain when privacy or throughput dominates.

The main limitation is cross-domain consistency because bridging state creates additional failure modes and latency and security risks.

Key points- Keep PII and high-churn app state off-chain for privacy and speed

- Put settlement, ownership and policy rules on-chain as a shared source of truth

Learn more: Off-Chain On-Chain Hybrid Finance Stack Opens in the same page.

-

Stablecoins are typically privately issued tokens designed to track fiat value, tokenized deposits are bank liabilities represented as tokens and CBDCs are central bank issued digital money. Choose based on who carries credit risk and what settlement finality you need and which permissioning and compliance model fits your jurisdiction and counterparties.

The constraints differ across redemption guarantees and privacy and programmability and interoperability and the legal regime can change faster than the technology.

Key points- Stablecoins are private liabilities, tokenized deposits are bank deposits and CBDCs are central bank money

- Choose based on issuer risk, access model and compliance requirements

Reference: Stablecoin Tokenized Deposit CBDC

-

AI agent guardrails are policy, security and runtime controls that validate intent and constraints before any transaction is signed. Implement a policy engine with allowlists and limits and counterparty checks and simulation then separate proposing from signing via controlled signers like MPC or HSM with step-up approvals.

Even with controls you must assume model error and prompt manipulation so continuous monitoring and audit logs and incident response and kill switches remain mandatory.

Key points- Enforce least privilege with tool allowlists and scoped signing rights

- Require simulation with limits on size, frequency, slippage and time windows

Reference: Guardrails AI Agents Payments Trading Safe

-

Hybrid Finance is a mixed architecture that combines regulated Web2 rails with on-chain settlement and programmability, while DeFi is primarily on-chain finance driven by smart contracts and open liquidity, and traditional banking runs on centralized regulated ledgers. Choose Hybrid Finance when you need bank grade compliance and low latency UX but still want verifiable settlement, choose DeFi when open on-chain composability is the product, and choose traditional rails when jurisdiction, counterparties, and operational constraints dominate.

The tradeoffs are custody and compliance perimeter design in Hybrid systems, smart contract and liquidity risk in DeFi, and slower settlement and limited programmability in traditional banking.

Key points- DeFi is on-chain first, banking is closed-ledger first and hybrid splits responsibilities

- Pick hybrid for mainstream UX with compliance plus shared settlement guarantees

Learn more: Hybrid Finance DeFi Traditional Banking Opens in the same page.

-

A tokenized deposit is a bank deposit represented as a token where the token remains a direct claim on the issuing bank under a deposit style liability framework. Banks prefer it when they want programmability and faster settlement while keeping compliance, controls, and redemption inside their regulated operating model and balance sheet.

The limitations are permissioned access, reduced interoperability versus open stablecoin rails, and concentration of operational and credit risk at the issuing bank.

Key points- A tokenized deposit is on-chain representation of regulated bank deposit liabilities

- Banks prefer it for familiar compliance controls and client onboarding processes

Reference: Tokenized Deposit Banks Stablecoin

-

Transaction simulation and approvals for agentic systems is a control pattern where an agent proposes an action, the system simulates outcomes against policies, and a separate signer approves and executes the transaction. Use it when agents can initiate payments, trades, or treasury moves and you need deterministic policy enforcement with audit logs and step up approvals for higher risk actions.

The main risks are state drift between simulation and execution, policy misconfiguration, and prompt or tool manipulation so you still need strict limits, monitoring, and kill switches.

Key points- Split flow into intent, plan and execute so users approve outcomes

- Simulate effects, fees and risk impact and show a readable diff

FinTech Glossary 2026 20

- Stablecoin Rail

- A payment and settlement path that uses stablecoins as the value unit and blockchain transactions as the transfer primitive across wallets, custodians and platforms.

- Central Bank Digital Currency

- A digital form of sovereign money issued by a central bank, typically designed for regulated circulation, programmability controls and auditable compliance.

- Real-Time Payments

- A payments scheme that clears and confirms transfers within seconds, enabling continuous business operations instead of batch windows.

- Real-Time Settlement

- A settlement mode where final ledger movement happens near immediately rather than T+1 or T+2, reducing liquidity buffers but raising uptime and monitoring requirements.

- Correspondent Banking

- A cross-border model where banks route payments through intermediary banks, often introducing multi-hop delays, fees and operational reconciliation overhead.

- SWIFT Messaging Layer

- A standardized financial messaging network used to coordinate payment instructions and confirmations between institutions, separate from the actual movement of value.

- Atomic Swap

- A transaction pattern that exchanges assets between parties as a single all-or-nothing operation, preventing partial execution states.

- Delivery-versus-Payment (DvP)

- A settlement rule that couples asset delivery and payment so that neither leg completes without the other, reducing counterparty and settlement risk.

- Off-Chain Batching

- A throughput optimization that aggregates multiple actions off-chain before committing a smaller number of transactions on-chain, lowering fees and increasing effective TPS.

- Private L2

- A controlled Layer 2 environment where participants and data access are permissioned, designed to combine scalability with enterprise compliance constraints.

- Deterministic Finality

- A finality property where a transaction is considered irreversible once committed, with no probabilistic reorg risk after confirmation.

- Probabilistic Finality

- A finality model where confidence increases with more confirmations, but absolute irreversibility is not immediate due to possible chain reorganizations.

- Event Indexing

- A data pipeline that reads blockchain events and materializes them into queryable off-chain storage, supporting reporting, monitoring and product UX.

- Nonce Synchronization

- A coordination mechanism that prevents transaction collisions and ordering errors when multiple systems submit transactions from the same account.

- Gas Fee Estimation

- A runtime process that predicts the fee needed for timely inclusion of a transaction, balancing cost targets with confirmation latency requirements.

- Multi-Party Computation (MPC) Custody

- A key management approach where private key material is split across multiple parties or devices, so a single compromise does not expose signing authority.

- Permissioned Transfers

- A token transfer policy where sender and recipient must satisfy predefined access rules such as allowlists, jurisdiction checks or role constraints.

- Open Banking API

- A regulated API interface that exposes account and payment capabilities to authorized third parties, typically built around consent, strong customer authentication and audit logs.

- Anomaly Detection in Payment Flows

- A risk control layer that scores behavioral outliers in transaction streams and routes suspicious cases to step-up verification or manual review.